Why Your Estate Plan Needs a Smarter Return Strategy

What if your estate planning could do more than just pass on assets—but actually protect and grow them for future generations? I’ve seen too many families assume their wealth is safe, only to face unexpected losses. It’s not just about who inherits what; it’s about ensuring value endures. The real game-changer? Building a strategy that prioritizes long-term stability with realistic return expectations—without crossing into risky promises. Too often, people focus solely on legal documents like wills or trusts, believing these alone secure their legacy. But without thoughtful financial design, even the most carefully drafted plan can falter under the pressures of inflation, taxation, and poor investment choices. The difference between a plan that merely transfers wealth and one that sustains it lies in how returns are integrated into the structure from the start.

The Hidden Risk in Traditional Estate Planning

Traditional estate planning often centers on legal tools—wills, trusts, powers of attorney, and healthcare directives. While these are essential, they typically treat assets as static entities to be divided at death. This approach overlooks a critical reality: wealth does not exist in a vacuum. Over time, the purchasing power of money erodes due to inflation. A dollar today may be worth only forty cents in twenty years, depending on economic conditions. Without a strategy for asset growth, an estate can shrink in real value even if its nominal amount stays the same. Many families are surprised to learn that their loved one’s estate lost ground over time, not because of mismanagement, but because it was never designed to generate returns.

Another often-overlooked factor is taxation. Estate taxes, inheritance taxes, and capital gains taxes can significantly reduce what beneficiaries ultimately receive. For example, if an individual holds appreciated stock within their estate, selling it after death may trigger substantial tax liabilities unless planned for in advance. Additionally, poor asset allocation—such as keeping too much in low-yielding savings accounts or overly concentrated positions—can hinder long-term performance. These issues are not signs of failure; they are symptoms of a planning model that stops at legal formalities and ignores financial dynamics.

The solution is not to abandon traditional estate tools, but to enhance them with a financial strategy that anticipates change. Instead of viewing estate planning as a one-time event, it should be seen as an ongoing process that includes investment oversight, periodic rebalancing, and performance monitoring. By integrating return objectives into the plan, families can ensure that assets not only survive but thrive across generations. This shift requires a mindset change—from simply transferring wealth to actively stewarding it.

Why “Guaranteed Returns” Are a Myth (And What to Focus On Instead)

The promise of guaranteed returns is one of the most persistent myths in financial planning, especially within estate-related products. Insurance companies often market certain policies—such as indexed universal life or fixed annuities—as offering “guaranteed growth” or “market participation without risk.” While these products may have valuable features, it’s important to understand that no investment is truly risk-free. What appears to be a guarantee often comes with limitations, fees, or complex structures that reduce actual returns over time. Relying on such promises can lead to disappointment and missed opportunities for better-performing, transparent investments.

True financial security does not come from chasing unrealistic assurances, but from building a foundation of capital preservation and risk-adjusted growth. Capital preservation means protecting the principal value of assets, especially as one approaches or enters retirement. This doesn’t mean avoiding all risk—it means managing risk intelligently. For instance, a portfolio that includes high-quality bonds, dividend-paying equities, and cash equivalents can offer stability while still generating modest growth. The goal is not to double your money quickly, but to avoid large losses that are difficult to recover from.

Liquidity is another key consideration. An estate that is overly tied up in illiquid assets—such as non-income-producing real estate or private investments—can create challenges for beneficiaries who may need access to funds. A smarter approach balances liquidity with long-term appreciation potential. Professional planners focus on consistency, not hype. They build portfolios that aim for steady, compounding returns over decades, rather than speculative gains in a single year. This philosophy aligns with the long-term nature of estate planning, where small, reliable gains can make a significant difference over time.

Building Assets That Work After You Step Back

Estate planning should not be about freezing wealth in place, but about creating assets that continue to function independently. The most effective legacies are built on income-producing investments that generate ongoing value. Dividend-paying stocks, for example, can provide a stream of cash flow that benefits heirs without requiring them to sell shares. Companies with a history of increasing dividends over time—often referred to as “dividend aristocrats”—can offer both income and long-term growth potential. When structured properly within a trust or custodial account, these holdings can support multiple generations.

Real estate investments are another powerful tool. Rental properties, when well-managed, produce regular income and may appreciate in value over time. Unlike speculative real estate ventures, income-generating properties offer predictable cash flow that can help cover expenses, fund education, or support lifestyle needs for beneficiaries. Moreover, real estate can be held within legal structures like limited liability companies (LLCs) or family limited partnerships (FLPs), which provide liability protection and facilitate smooth transitions of ownership.

Structured bonds and other fixed-income instruments also play a role. Municipal bonds, for instance, may offer tax-free income, which can be especially valuable in high-tax states. Treasury Inflation-Protected Securities (TIPS) help preserve purchasing power by adjusting with inflation. These assets, when combined thoughtfully, create a diversified income engine that operates even when the original planner is no longer involved. The key is to design the portfolio with both current and future needs in mind, ensuring that it serves its purpose across different life stages.

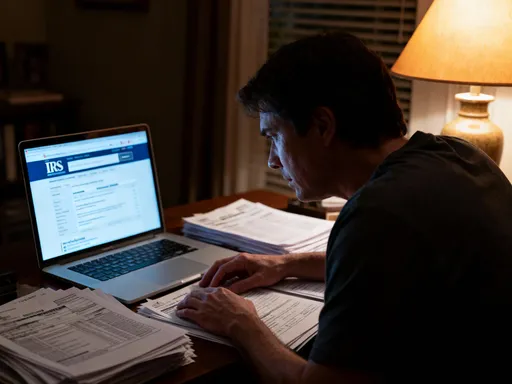

Tax Efficiency: Keeping More of What You Built

Taxes are one of the largest silent threats to inherited wealth. Without proactive planning, a significant portion of an estate can go to federal and state governments rather than to the intended beneficiaries. The federal estate tax exemption is substantial—over $12 million per individual as of recent years—but it is subject to change based on legislation. Even for estates below the threshold, state-level inheritance or estate taxes may apply. Capital gains taxes are another concern, particularly when beneficiaries inherit appreciated assets like stocks or real estate.

One of the most effective strategies for reducing tax exposure is gifting during life. The IRS allows individuals to gift up to a certain amount each year per recipient without triggering gift tax reporting. Over time, this can transfer substantial wealth while removing future appreciation from the taxable estate. For example, gifting shares of a growing company today means that all future gains occur outside the estate, potentially saving millions in taxes. These gifts can be made directly or through trusts designed to maximize tax benefits, such as irrevocable life insurance trusts (ILITs) or grantor retained annuity trusts (GRATs).

Trust structures also offer powerful tax advantages. A properly structured trust can control when and how assets are distributed, while minimizing tax consequences. For instance, a trust can be designed to distribute income annually, allowing beneficiaries to pay taxes at their own rates, which may be lower than the trust’s rate. Additionally, timing matters. Transferring assets before a major appreciation event—such as a company sale or real estate boom—can lock in lower valuations and reduce future tax liability. These strategies require careful coordination with tax professionals, but the savings can be transformative for heirs.

Balancing Risk Without Sacrificing Growth Potential

One of the most common pitfalls in late-stage financial planning is misjudging risk tolerance. On one end of the spectrum, some individuals become overly conservative, moving all their assets into low-yield savings accounts or certificates of deposit. While this may feel safe, it often fails to keep pace with inflation, effectively eroding wealth over time. On the other end, some take on excessive risk in pursuit of high returns, investing in speculative ventures or concentrated positions that could result in significant losses. The goal is not to eliminate risk, but to manage it in a way that aligns with long-term objectives.

A balanced approach uses diversified portfolios tailored to different life stages. During the wealth accumulation phase—typically before retirement—the focus is on growth-oriented assets like equities. As one transitions into the wealth preservation and transfer phase, the allocation gradually shifts toward more stable, income-producing investments. This evolution is not about abandoning growth, but about prioritizing consistency and capital protection. For example, a 70-year-old may hold a mix of 50% equities (including dividend payers), 40% bonds, and 10% alternatives, whereas a 40-year-old might have 80% in equities.

Asset location is also important. Not all accounts are taxed the same way, so placing certain investments in tax-advantaged accounts—like IRAs or 401(k)s—can enhance after-tax returns. For instance, holding bonds in a tax-deferred account and equities in a taxable account may be more efficient due to the different tax treatment of interest income versus capital gains. This level of detail reflects the sophistication needed in modern estate planning, where financial decisions have lasting legal and tax implications.

Tools and Structures That Support Long-Term Value

Legal structures are not just about control and distribution—they can also enhance financial performance. Irrevocable trusts, for example, remove assets from the taxable estate while allowing for managed growth. Once assets are transferred into an irrevocable trust, they are no longer owned by the individual, which can reduce estate tax liability. At the same time, the trust can be designed to invest in income-producing assets, ensuring that the wealth continues to grow for beneficiaries. The grantor can even retain certain rights, such as the ability to receive income from the trust, depending on the structure.

Family limited partnerships (FLPs) are another valuable tool. These entities allow families to pool assets—such as real estate or investment portfolios—under a single management structure. The older generation typically holds general partnership interests, maintaining control, while younger members receive limited partnership shares as gifts. This not only facilitates wealth transfer but also provides valuation discounts for tax purposes, since limited interests are less liquid and carry fewer rights. Over time, this can result in significant tax savings.

Beneficiary designations on retirement accounts and life insurance policies are often overlooked, yet they play a crucial role in estate planning. These designations override wills, meaning that even the most carefully written document cannot change who receives the assets. Naming the right beneficiaries—and updating them regularly—is essential. For example, using a “conduit trust” as a beneficiary of an IRA can protect the funds from creditors, divorce, or poor spending habits, while still allowing for stretch distributions over the beneficiary’s lifetime. These tools, when used correctly, turn estate planning from a passive transfer into an active wealth management strategy.

The Role of Professional Guidance in Sustainable Planning

No matter how informed an individual may be, estate planning involves complex interactions between law, tax, and finance. Attempting to navigate these areas without expert help can lead to costly mistakes. For example, a poorly drafted trust may fail to achieve its tax objectives, or a misplaced beneficiary designation could disinherit a child unintentionally. This is why involving qualified professionals is not a luxury—it’s a necessity. Financial advisors, tax attorneys, and fiduciary planners each bring specialized knowledge that ensures the plan works in practice, not just on paper.

Coordination among these professionals is equally important. A financial advisor may recommend an investment strategy, but without input from a tax attorney, the tax consequences may be overlooked. Similarly, an estate attorney may draft documents that don’t align with the client’s financial goals. The most effective plans emerge from collaboration, where all parties work together to create a unified strategy. This team-based approach ensures that every decision—from asset allocation to trust funding—is aligned with the client’s values and long-term vision.

Professional guidance also provides accountability and continuity. Life changes—marriage, divorce, birth, death, relocation—can all impact an estate plan. Regular reviews with advisors ensure that the plan evolves with these changes. Moreover, having a trusted team in place makes it easier for families to manage the estate after the planner’s passing, reducing confusion and conflict. In this way, professional involvement doesn’t just improve outcomes—it brings peace of mind.

Estate planning should never be a one-time document signed and forgotten. True legacy building means designing a system where wealth continues to serve your values long after you're gone. By focusing on sustainable returns, tax-smart moves, and risk-aware strategies, you’re not just passing on money—you’re passing on security, opportunity, and peace of mind. The most enduring legacies are not measured by size, but by impact. When assets are structured to grow, protect, and provide, they become more than an inheritance—they become a foundation for future success. With thoughtful planning and expert support, your estate can do more than survive. It can thrive.